On 18 March, the Science Based Targets Initiative (SBTi) – a global standard setter helping companies set emissions targets aligned with climate science – published its highly anticipated 132-page “initial consultation” document describing proposed revisions to its Corporate Net Zero Standard.

SBTi is assembling five working groups to input into key revisions and will take feedback through its online consultation until 1 June 2025. Climate Impact Partners will respond to the consultation, and we welcome clients to join our in our response.

Register your interest to be part of our consultation response

If you are interested in being included in our response, please let us know.

Nothing in the draft is final. However, the updates point towards a direction of travel, particularly regarding the use of carbon credits on the road to Net Zero. This article provides:

- An overview of the key updates

- How they compare with SBTi’s current Corporate Net Zero Standard (V1.2)

- What this could mean for the role of carbon credits in net zero strategies

- The growing recognition of beyond value chain mitigation (BVCM)

Alternatively, watch our webinar with Claims and Assessment Director, Chris Duck, and Product Development Manager, Shachar Hatan, and PR and Communications Director, Hannah Blackmore, for expert insights on these updates.

Corporate Net Zero Standard V2 Milestones

- March 2025: Draft Net Zero Standard V2.0 released for consultation.

- June 1, 2025: Deadline for Net Zero Standard V2.0 consultation feedback.

- Late 2025 / 2026: Launch of Net Zero Standard V2.0 Note: V1.2 will remain valid for 5 years, or until the end of 2030, whichever comes first.

- 2027+: Implementation and use of Net Zero Standard V2.0.

SBTi Corporate Net Zero Standard V2

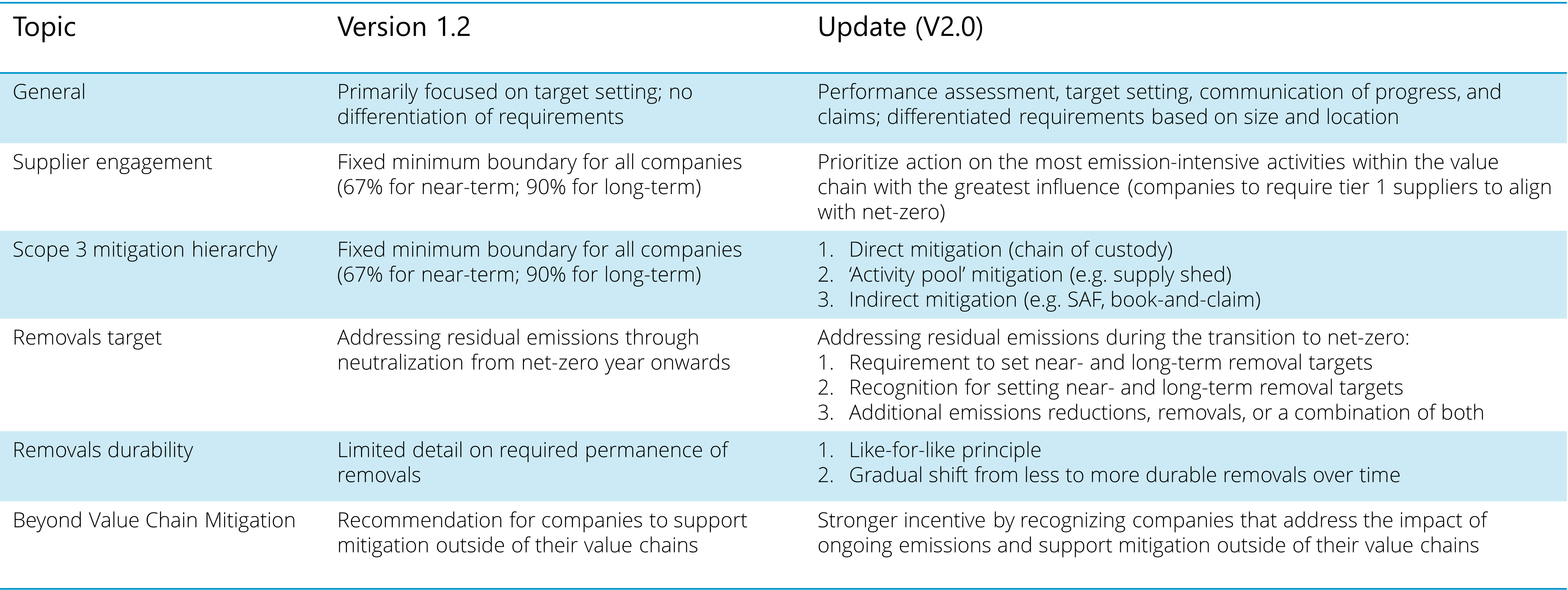

The Science Based Targets initiative (SBTi) is expanding its focus in Version 2.0, moving beyond just target setting to include performance assessment, communication of progress, and claims, with considerations for company size and geographic location.

The draft update covers key areas impacting the use of carbon credits and market instruments, including:

- Supplier Engagement

- The Mitigation Hierarchy for Scope 3 Emissions

- The Introduction of Removals Targets

- The Emphasis on Removals Durability

- The Formal Recognition of Beyond Value Chain Mitigation (BVCM)

Supplier Engagement

The SBTi proposes requiring (or potentially recommending) companies to engage their tier 1 suppliers in setting their own net-zero targets. Tier 1 suppliers are those with direct contractual obligations to the reporting company. This initiative aims to drive decarbonization across Scope 3 emissions through influence, prioritizing emissions-intensive activities. This signifies a push to extend mitigation efforts beyond direct operations, potentially increasing demand for carbon removals and nature based solutions as suppliers pursue their own emissions reductions. The SBTi acknowledges the challenge with supplier engagement of this scale and is therefore looking at the feasibility of this requirement.

Mitigation Hierarchy for Scope 3

The new guidance introduces recognition and acknowledgement of "indirect mitigation" measures and "supply shed" concepts, addressing the complexities of Scope 3 emissions.

- Direct mitigation: Interventions linked to specific emissions sources within the company’s value chain through a chain of custody model.

- ‘Activity pool’ / supply shed mitigation: Emissions sources physically serving the company but lacking individual traceability. This acknowledges the challenges of progressing against targets when physical traceability is unclear, potentially referencing "insetting" projects within the supply chain.

- Indirect mitigation: Measurable net-zero-aligned transformations relevant to the company’s value chain, comparable to direct mitigation, but lacking a physical connection. Examples include Sustainable Aviation Fuel contracts or certificates. Quality and traceability criteria will be defined.

This nuanced approach to Scope 3 mitigation may influence how companies utilize carbon credits, emphasizing the importance of clear traceability and quality assurance. This may also allow for implementation of insetting projects which deliver reductions in the value chain, where physical traceability is not clear.

Removal Targets

A significant shift is the introduction of a "Removals Target" for Scope 1 emissions. Scope 2 and Scope 3 emissions are excluded from the removals target.

- Option 1: Requires interim removal milestones, gradually increasing to match 100% of Scope 1 residual emissions with carbon dioxide removals (CDR) at the net-zero year.

- Option 2: Recommends setting additional removal targets, with formal recognition for doing so.

- Option 3: Offers flexibility to address the final 10% of residual emissions through either removals or further abatement.

This focus on carbon removals signals a growing recognition of their crucial role in achieving net-zero, potentially driving increased demand for high-quality removal credits. Purchase of removal-type carbon credits may represent the removals included within this target. It is very important to note that the SBTi still requires 100% of residual emissions across all scopes to be compensated at net zero.

Removals Durability

The SBTi proposes a minimum durability threshold for carbon removals, emphasizing long-term storage.

- Option 1: "Like-for-like" matching of residual emissions by greenhouse gas type with equivalent CO₂ storage duration. For example, fossil fuel-based CO₂ requires 1,000-year permanence removals, whereas other greenhouse gases such as methane and nitrous oxide require 12-120-year durability.

- Option 2: A "gradual transition" approach, requiring a shift from less to more durable removals between 2030 and 2050, without needing to break down emissions by type.

This focus on durability indicates a potential shift towards geological storage and other novel durable removal methods. However, the SBTi acknowledges that nature-based removal methods continue to play an important role owing to their cost-competitiveness, contributing significantly to near-term mitigation. These considerations will influence the demand for various carbon removal technologies and nature-based solutions.

Beyond Value Chain Mitigation (BVCM)

The SBTi proposes formal recognition for delivering mitigation activities beyond the value chain, known as beyond value chain mitigation (BVCM), to address the impact of ongoing emissions. BVCM encompasses activities that reduce or remove emissions outside of a company’s value chain.

Companies are expected to take responsibility for all Scope 1 and 2 emissions and part or all of Scope 3.

BVCM contributions can be annual or at the end of target cycles.

The SBTi recommends:

- Addressing 100% of ongoing emissions if using carbon credits.

- Accounting for historic emissions.

- Prioritizing activities that provide substantial co-benefits, particularly those delivered through nature-based solutions.

This emphasis on BVCM highlights the growing recognition of the role companies can play in supporting broader climate action, potentially driving demand for high-quality carbon credits with strong co-benefits.

Learn how we helped Deloitte North and South Europe (NSE) to deliver an innovative program aligned with SBTi’s BVCM framework.

Summary of Changes

Get in touch with our global expert team

Get in touch if you want to discuss how these changes may impact your organization