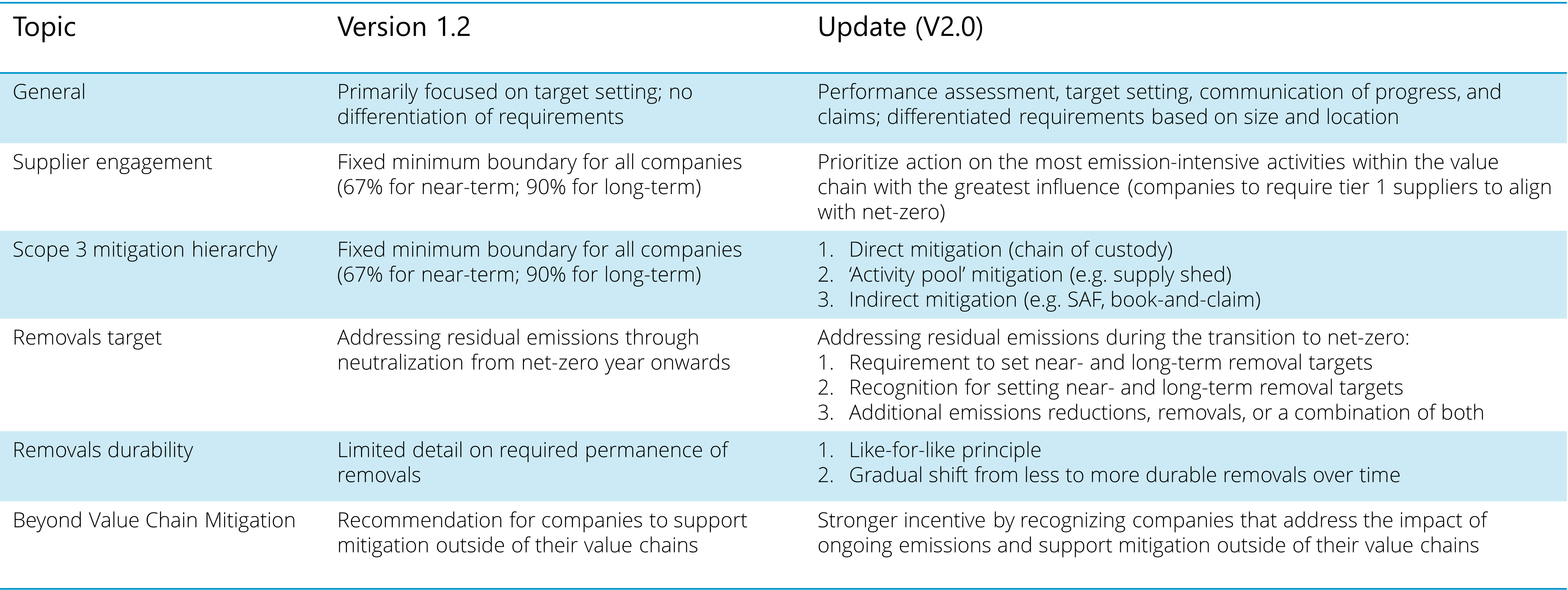

Launched in 2021 (V1.0, now V1.2), the SBTi's Corporate Net-Zero Standard provides a framework for businesses to set validated, science-based targets on their path to achieving net-zero emissions, aligned with the Paris Agreement. Driven by the urgency of the climate crisis and the latest scientific understanding, more substantial changes have been outlined in the draft V2.0 - out for consultation until 1 June 2025.

This Q&A addresses your top questions about the SBTi's Corporate Net Zero Standard V2.0.

For a deeper dive, watch our recent webinar recording or read our insights article - Navigating the SBTi's Proposed Net-Zero Revisions.

-

Nothing in the draft is final. However, the updates point towards a direction of travel, particularly regarding the use of carbon credits on the road to Net Zero.

Watch our webinar with Claims and Assessment Director, Chris Duck, and Product Development Manager, Shachar Hatan, and PR and Communications Director, Hannah Blackmore, for expert insights on these draft updates.

-

See the timeline below to understand when the proposed changes may come into effect.

-

- The SBTi will provide clarity on how organisations will need to transition to the new standard in the future.

- For companies with existing near-term targets the current standard, V1.2, should remain valid for five years or until the end of 2030 – whichever comes first. The SBTi has committed to providing further details to companies with previously validated near-term targets later in 2025.

- For companies seeking to set new near-term targets i.e. for 2030 in the years 2025 and 2026, they will be able to set them under Version 1.2. From 2027 onwards, companies will use Version 2.0 to set new near term and long term targets. Targets set in 2025 and 2026 will remain valid for five yar, or until the end of 2030 – whichever comes first.

-

One of the aims is to reduce the burden of additional reporting and ensure alignment across frameworks. The intention is to balance robustness and credibility without overburdening companies, and there is ongoing consultation and iteration to ensure that.

The comments that the SBTi receives as part of the consultation are likely to have an influence.

Supply Chain & Supplier Obligations

The SBTi proposes requiring (or potentially recommending) companies to engage their tier 1 suppliers in setting their own net-zero targets. This initiative aims to drive decarbonization across Scope 3 emissions through influence, prioritizing emissions-intensive activities.

-

A Tier 1 supplier is a company that directly provides goods or services to the customer, forming the closest level of the supply chain. These supplier have direct business relationships and contracts with the company, meaning they purchase directly from them.

-

Yes, this concern was acknowledged by the SBTi, with the importance of providing support to smaller suppliers emphasized. The SBTi understands that for some suppliers, especially in hard-to-abate sectors, setting targets will be more difficult. This is why timelines, sector-specific guidance, and capacity building are critical.

-

The SBTi recognizes this challenge and is developing sector-specific pathways, such as for cement, steel, and aviation. These pathways account for technological readiness and allow for tailored transition strategies. The importance of feasibility and realistic timelines was emphasized.

Mitigation Hierarchy for Scope 3 Emissions

The new guidance introduces recognition and acknowledgement of "indirect mitigation" measures and "supply shed" concepts, addressing the complexities of Scope 3 emissions.

-

The SBTi is proposing three approaches for addressing supply chain emissions (scope 3), in an order of priority:

- Direct mitigation: interventions that can be linked to specific emissions sources in the company’s value chain through a chain of custody model.

- ‘Activity pool’ / supply shed mitigation: emissions sources that may physically serve the company but lack physical traceability to individual sources. This concept may allow ‘insetting’ mitigation projects to be more easily acknowledged as part of value chain abatement.

- Indirect mitigation: measurable net-zero-aligned transformation relevant to a company’s value chain and comparable to direct mitigation but lack a physical connection to the reporting company’s value chain (e.g. Sustainable Aviation Fuel, other book-and-claim).

-

Further clarity is needed from the SBTi with regards to insetting in the final version of the new Net Zero Standard. The ‘supply shed’ concept could allow for recognition of abatement from insetting projects, even where there is no physical traceability of a product in the value chain.

Insetting is when a company embeds projects within its own supply chain to reduce or remove greenhouse gas emissions, for example, Nespresso, an operating unit of the Néstle group, has implemented regenerative agriculture as part of their insetting journey. Coffee plantations flourish when grown in shade, so the company has invested in tree planting within the coffee farms and surrounding landscape (source World Economic Forum).

A book and claim system allows a company to book the environmental benefits of a sustainable product, such as Sustainable Aviation Fuel (SAF) and then claim those benefits.

-

- Carbon avoidance credits, or other types of carbon credits, will be more formally recognised as a mitigation activity against ‘ongoing emissions’, through Beyond Value Chain Mitigation initiatives.

- Avoidance credits will not be used to compensate residual emissions at net zero.

-

The SBTi is exploring the acknowledgement of market based mechanisms in recognizing abatement. Further clarity on their treatment under the current standard is required, and companies should consult with the SBTi in the meantime. The GHG Protocol is undergoing a review process to give guidance on the treatment of market instruments in GHG accounting methodologies, due to the current lack of clarity.

-

The SBTi plans to align with robust, credible frameworks and criteria, such as the ICVCM (Integrity Council for the Voluntary Carbon Market) and the Oxford Offsetting Principles. The aim is to avoid subjectivity by setting science-based guardrails and being transparent about criteria.

Carbon Removals Targets

A significant shift is the introduction of a "Removals Target" for Scope 1 emissions. Scope 2 and Scope 3 emissions are excluded from the removals target.

-

- Carbon credits can be used as part of the proposed ‘removals target’ and BVCM activities, in addition to the compensation of residual emissions through removals as at net zero.

- Carbon credits cannot be used to contribute towards abatement (reduction) of the greenhouse gas GHG inventory of an organization.

-

The SBTi is likely to provide more information on allowable carbon credits in the final version of the standard, such as allowable standards or quality criteria, e.g. the use of CCP-labelled credits.

In the draft the SBTi gave guidance on potential treatment of removals durability as follows:

- The like-for-like approach (emissions are categorized by greenhouse gas type, requiring targeted removal methods that correspond to an equivalent CO₂ storage duration, therefore allowing for both biosphere and geosphere removals); and

- The gradual transition approach (from less to more durable removal, meaning gradually transitioning from biosphere to geosphere removals).

-

For example, if in a given year a company reduces emissions by 3% and also purchases Scope 1 removals for 1%, will they be able to claim a 4% improvement towards their net-zero target that year?

- No, carbon credits cannot be counted towards an abatement target.

- Carbon credits contributing to the removals target or BVCM activities are separate from the abatement requirements of an organisation.

-

SBTi is clear that it does not allow carbon credits (often called offsets) to count as a reduction in an organization’s GHG inventory, as a substitute or replacement for abatement.

However, carbon credits have the following uses under SBTi’s draft standard:

- The proposed removals target

- Beyond Value Chain Mitigation (BVCM) on the pathway to net zero

- Compensation of residual emissions at the point of net zero

-

Companies can use carbon credits to remove or avoid emissions on the pathway to net zero, which SBTi calls Beyond Value Chain Mitigation (BVCM). Organizations could choose to deliver BVCM outcomes using carbon credits in addition to the removals target and the SBTi is considering whether the removals target will be mandatory or recommended.

-

The removals target is a gradual increase of removals over time until 100% of residual Scope 1 emissions is matched by the net zero year. It’s possible that if target Scope 1 emissions are expected to be zero at the net zero year, then the removals target will also be zero.

See the graph below.

-

Not that we are aware of - and both options are on the table to be considered. Based on the feedback we hear from our clients, we expect users of the Net Zero Standard will look for pragmatism and lower complexity, which may favour the 'optional' route for the removals target, and transitional durability route.

-

We expect the VCM demand to increase due to:

- Further guidelines on durable removals, and

- The emphasis and recognition for BVCM.

As demand rises and supply remains constrained, higher numbers of buyers are expected to secure future access to credits through longer-term agreements. This is of course a stronger signal if it becomes a mandatory requirement, however, even as a recommendation it is a clear endorsement from the SBTi that companies should be taking responsibility beyond the value chain for emissions today on the pathway to net zero.

-

The impact of carbon credits are measured in ‘tonnes CO2e’ which takes into account durability of different greenhouse gases.

This scenario is considered and addressed as part of the durability thresholds for removals. According to the like-for-like approach, since methane emissions are short-lived (12 years), they can be targeted using less durable methods such as nature-based removals with a 100-year durability, rather than geosphere removals of 1000-year durability.

Additional Recognition & Beyond Value Chain Mitigation

The SBTi proposes formal recognition for delivering mitigation activities beyond the value chain, known as Beyond Value Chain Mitigation (BVCM), to address the impact of ongoing emissions. BVCM encompasses activities that reduce or remove emissions outside of a company’s value chain.

-

The most common way of contributing outside of the value chain is by purchasing high quality carbon credits. There are other options, which include investing in nascent technologies to advance climate mitigation in the future.

-

The guidance is clear that companies should focus on reducing Scope 1, 2, and 3 emissions in line with science before relying on BVCM (Beyond Value Chain Mitigation):

- BVCM is important, as it supports the crucial transition to net zero, including scale up of nascent solutions, but should be additional to strong internal reduction efforts.

- The sequencing is crucial, with internal abatement as a priority.

-

The concept of “additional recognition” is under discussion. The idea is to provide space for companies to get credit for BVCM without it being a substitute for internal reductions. Some suggestions included public acknowledgment, registry features, or differentiated scoring.

-

For ongoing emissions, i.e. on the journey to reach net zero, companies are recommended to contribute to BVCM activities, most commonly through the purchase of high quality carbon credits, according to their levels of ongoing emissions (i.e. Scopes 1,2,3 at any given time until the net zero year).

For residual emissions, the last 10% that cannot be further abated, at the net-zero year, companies should purchase carbon removal credits with the appropriate durability threshold (based on the like-for-like approach or the gradual transition approach).